PowerPoint-Präsentation

... Expected return is too high. Investors bid up price until expected return falls. individual stock or portfolio lies below SML: Expected return is too low. Investors sell stock driving down price until expected return rises. Fußzeile ...

... Expected return is too high. Investors bid up price until expected return falls. individual stock or portfolio lies below SML: Expected return is too low. Investors sell stock driving down price until expected return rises. Fußzeile ...

Far East Hospitality Trust - Singapore

... believe there are limited re-rating catalysts for the stock in the near term. Key Risks: Interest rate risk. Any increase in interest rates will result in higher interest payments that the REIT has to make annually to service its loans. This reduces the income available for distribution, which will ...

... believe there are limited re-rating catalysts for the stock in the near term. Key Risks: Interest rate risk. Any increase in interest rates will result in higher interest payments that the REIT has to make annually to service its loans. This reduces the income available for distribution, which will ...

Slide 0 - Unicaja

... This document is not an offer for the sale of, or the solicitation of an offer to subscribe for or buy, any securities in the United States or to U.S. persons. Securities may not be offered or sold in the United States absent registration or an exemption from registration under the U.S. Securities A ...

... This document is not an offer for the sale of, or the solicitation of an offer to subscribe for or buy, any securities in the United States or to U.S. persons. Securities may not be offered or sold in the United States absent registration or an exemption from registration under the U.S. Securities A ...

Return on Capital Employed The ROCE Formula Calculating ROCE

... sum of adjusted net working capital and net fixed assets. Net working capital is typically defined as current assets less current liabilities. However, we take this one step further by narrowing our focus to accounts receivable, inventory and cash needed to conduct business less accounts payable. A co ...

... sum of adjusted net working capital and net fixed assets. Net working capital is typically defined as current assets less current liabilities. However, we take this one step further by narrowing our focus to accounts receivable, inventory and cash needed to conduct business less accounts payable. A co ...

Full Text PDF - Great Cities Institute

... The ability to protect of the quality of money and ensure the integrity of financial transactions have long been capacities at the center of any formal definition of state sovereignty (Arrighi, 1994; Dodd, 1995; Knafo, 2008). The development of these capacities has evolved through the advent of the ...

... The ability to protect of the quality of money and ensure the integrity of financial transactions have long been capacities at the center of any formal definition of state sovereignty (Arrighi, 1994; Dodd, 1995; Knafo, 2008). The development of these capacities has evolved through the advent of the ...

Systemic Risk and the Financial Crisis: A Primer

... “counterparty risk,” which is also known as “default risk.”10 Counterparty risk is the danger that a party to a financial contract will fail to live up to its obligations. Counterparty risk exists in large part because of asymmetric information. Individuals and firms typically know more about their ...

... “counterparty risk,” which is also known as “default risk.”10 Counterparty risk is the danger that a party to a financial contract will fail to live up to its obligations. Counterparty risk exists in large part because of asymmetric information. Individuals and firms typically know more about their ...

Statements of Accounting Standards (AS 10)

... 9.3 Administration and other general overhead expenses are usually excluded from the cost of fixed assets because they do not relate to a specific fixed asset. However, in some circumstances, such expenses as are specifically attributable to construction of a project or to the acquisition of a fixed ...

... 9.3 Administration and other general overhead expenses are usually excluded from the cost of fixed assets because they do not relate to a specific fixed asset. However, in some circumstances, such expenses as are specifically attributable to construction of a project or to the acquisition of a fixed ...

Factors affecting the price of catastrophe bonds

... different types of bonds 9 Helps to separate the effect of the different factors 9 People are not very good at separating random effects from a real trend. They can be easily “fooled by randomness” 9 Gives estimates about the errors in our estimates 8 Subjective choice of model 8 Trends may be hidde ...

... different types of bonds 9 Helps to separate the effect of the different factors 9 People are not very good at separating random effects from a real trend. They can be easily “fooled by randomness” 9 Gives estimates about the errors in our estimates 8 Subjective choice of model 8 Trends may be hidde ...

Section 1

... the collateral which bears a reasonable relationship to the plan’s outstanding credit at a particular moment (e.g., collateral with a value equal to 150% of the outstanding credit) should be treated as assets of the credit provider, but any collateral in excess of that amount should continue to be r ...

... the collateral which bears a reasonable relationship to the plan’s outstanding credit at a particular moment (e.g., collateral with a value equal to 150% of the outstanding credit) should be treated as assets of the credit provider, but any collateral in excess of that amount should continue to be r ...

MYLAN LABORATORIES INC

... products, two of which were launched in late March 1996 and one which was added during the quarter ended June 30, 1996. Research and development expense of $10,531,000 for the current quarter represents a 29% increase over the prior year first quarter. The current quarter amount is consistent with e ...

... products, two of which were launched in late March 1996 and one which was added during the quarter ended June 30, 1996. Research and development expense of $10,531,000 for the current quarter represents a 29% increase over the prior year first quarter. The current quarter amount is consistent with e ...

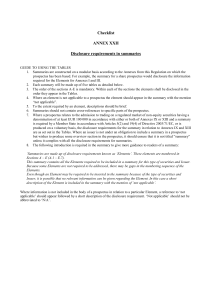

Checklist ANNEX XXII Disclosure requirements in summaries

... characteristics that demonstrate capacity to produce funds to service any payments due and payable on the securities a description of the general characteristics of the obligors and in the case of a small number of easily dentifiable obligors, a general description of each obligor a description ...

... characteristics that demonstrate capacity to produce funds to service any payments due and payable on the securities a description of the general characteristics of the obligors and in the case of a small number of easily dentifiable obligors, a general description of each obligor a description ...

Chapter 17

... • Reserves, Cash items in Process of Collection, and Deposits at Other Banks are collectively referred to as Cash Items in our balance sheet, and account for 2% of assets. ...

... • Reserves, Cash items in Process of Collection, and Deposits at Other Banks are collectively referred to as Cash Items in our balance sheet, and account for 2% of assets. ...

Fair Value: Fact or Opinion

... If life were simple, the value of an asset would be analyzed by looking at how an exactly identical asset - in terms of risk, growth and cash flows - is priced. Identical assets can be found with real assets or even with fixed income assets, but difficult to find with risky assets or businesses. In ...

... If life were simple, the value of an asset would be analyzed by looking at how an exactly identical asset - in terms of risk, growth and cash flows - is priced. Identical assets can be found with real assets or even with fixed income assets, but difficult to find with risky assets or businesses. In ...

Farm Financials Starting with Schedule F

... • Most of the entries are based on cash that came in or was paid out during the year • A big exception is depreciation, a non-cash expense that can vary a lot from year to year • It only pertains to the farm business; the farm family’s personal expenses aren’t included ...

... • Most of the entries are based on cash that came in or was paid out during the year • A big exception is depreciation, a non-cash expense that can vary a lot from year to year • It only pertains to the farm business; the farm family’s personal expenses aren’t included ...

Chapter 6: The Measurement Perspective on Decision Usefulness

... The focus of the chapter is to analyze if accounting information can be made more useful in decision-making by taking a more measurement orientated approach in financial reporting. The measurement perspective differs from the information perspective that has been presented in previous chapters. The ...

... The focus of the chapter is to analyze if accounting information can be made more useful in decision-making by taking a more measurement orientated approach in financial reporting. The measurement perspective differs from the information perspective that has been presented in previous chapters. The ...

DEPARTMENT OF LABOR AND EMPLOYMENT

... The purpose of proposed amendments to 1 CCR 210-1 is to define “outstanding debt,” to establish information to be provided to licensees, and to establish guidelines for the Gambling Intercept Cash Fund fee. The statutory basis for proposed amendments to 1 CCR 210-1 is found in section 24-35-601, et ...

... The purpose of proposed amendments to 1 CCR 210-1 is to define “outstanding debt,” to establish information to be provided to licensees, and to establish guidelines for the Gambling Intercept Cash Fund fee. The statutory basis for proposed amendments to 1 CCR 210-1 is found in section 24-35-601, et ...

IRAC 040413-RBI - College of Agricultural Banking

... interest accrued and credited to income account in the past periods should be reversed if the same is not realised. Applies to Government guaranteed accounts also - Fees, commission and similar income that have accrued should cease to accrue and past dues if uncollected to be reversed ...

... interest accrued and credited to income account in the past periods should be reversed if the same is not realised. Applies to Government guaranteed accounts also - Fees, commission and similar income that have accrued should cease to accrue and past dues if uncollected to be reversed ...

Self-Storage Industry Is Poised for More Growth

... managers for local operators. By serving in this capacity, REITs can expand into new markets and extend their brand names without deploying additional capital. The publicly traded REITs also have good access to all sources of public and private capital. Through their access to capital at rates that ...

... managers for local operators. By serving in this capacity, REITs can expand into new markets and extend their brand names without deploying additional capital. The publicly traded REITs also have good access to all sources of public and private capital. Through their access to capital at rates that ...

Setting aside the debate on when the exact date of an interest rate

... relative basis as interest rates rise, potentially leading to active manager out‐ performance. ...

... relative basis as interest rates rise, potentially leading to active manager out‐ performance. ...

glossary and abbreviations - ACT Department of Treasury

... (b) it is held primarily for the purpose of being traded; or (c) it is due to be settled within twelve months after the reporting date; or (d) the agency does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting date. ...

... (b) it is held primarily for the purpose of being traded; or (c) it is due to be settled within twelve months after the reporting date; or (d) the agency does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting date. ...

The Growing Role of Alternative Investments

... manage risk or achieve a reasonable return. Unlike fixed income investments, many alternatives are not as directly affected by interest rate changes and, as such, can provide both risk management and return enhancement benefits. ...

... manage risk or achieve a reasonable return. Unlike fixed income investments, many alternatives are not as directly affected by interest rate changes and, as such, can provide both risk management and return enhancement benefits. ...