Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

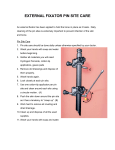

white paper Prepared by: Jeff Hall Director Technology Risk Management Services RSM McGladrey, Inc. jeff.hall@rsmi.com 612.376.9280 www.rsmmcgladrey.com white paper The purpose of this document is to explain the issues with Chip and PIN credit cards and their compliance with the PCI Data Security Standard. Background Chip and PIN is a British government-backed initiative to implement the Europay, MasterCard and Visa (EMV) standard for credit cards with a built-in integrated circuit (IC), also known as IC Cards or Chip and PIN. The purpose of Chip and PIN was to reduce the amount of fraud in face-to-face credit card transactions. Chip and PIN is a worldwide standard that has been extensively implemented in Canada and Europe, but has not been introduced into the United States or most of the Far East. With the exception of Discover Financial, all of the other major card brands (Visa, MasterCard, JCB and American Express) have adopted various forms of the Chip and PIN technology. How Chip and PIN works Chip and PIN replaces the magnetic stripe and receipt signing common in the United States. In Chip and PIN technology, the information normally contained on the magnetic stripe is recorded on an integrated circuit (IC) contained in the card. The data stored in the IC is encrypted using the DES, 3DES, RSA or SHA encryption algorithms. Rather than swiping the magnetic stripe, the card is inserted into the payment terminal where the IC is read and decrypted, and the transaction is generated for authorization. If authorized, cardholders are required to enter their PIN into the terminal, and then the receipt is generated and the transaction is completed. Chip and PIN terminals provide the capability of processing Chip and PIN cards, as well as having magnetic stripe readers. Chip and PIN terminals can operate over wired, dialup, 802.11 wireless or cellular networks. In all connectivity environments, the terminals use secure transmission technology to ensure the privacy of cardholder data. Potential security issues While Chip and PIN has significantly reduced fraud in face-to-face transactions, there are a number of issues regarding the security of this technology. The EMV specification is open source and available from a number of sources, including EMVCo. Because of this, attackers can obtain the specification to build their own hardware and software for creating and processing Chip and PIN cards, as well as creating attack methods to compromise the cards. This has lead to a number of successful attacks to the Chip Authentication Protocol/Dynamic Passcode Authentication (CAP/DPA) protocols, resulting in cloned cards, as well as obtaining and computing valid PINs. www.rsmmcgladrey.com Another concern is that the entry of the PIN can be bypassed by the merchant. If bypassed, a receipt is generated and signed by the cardholder — no different from a transaction performed with a traditional credit card. While European banks have tried to discourage this practice, this option is still available, which does not provide any additional protection against fraudulent transactions. Theft of physical credit cards has risen since the introduction of Chip and PIN technology. Criminals often hold victims hostage and threaten them with bodily harm until they reveal their PIN, which the criminals can confirm with a simple card reader. Card readers are easy to come by, as a number of UK banks flooded the market with card readers when the Chip and PIN cards were introduced. Banks encourage credit and debit card customers to take their card readers along with them. The readers require the entry of the PIN to get information displayed from the card. Security researchers found four keys on the customer’s card reader that were heavily used and worn which reduced the likelihood of guessing a card’s PIN from 1 in 3,333 to 1 in 8. Chip and PIN cards connected to PCs can generate authentication tokens, but the CAP/DPA standards do not specify how these tokens should be used in an online environment. In addition, not all e-commerce sites and banks have implemented this capability into their Internet processing environments. As a result, additional security of online environments is not enhanced by using Chip and PIN cards. Some banks will not allow their Chip and PIN cards to be used online. PINs are typically the same for both Chip and PIN cards and ATM/cash cards, if a person has both types issued by the same bank. As a result, if you know the PIN for one, you know it for both. Offline entry of PINs is supported by certain cards in certain countries. In offline mode, the PIN is not encrypted, so it can readily be retrieved in plain text from the terminal. A shift in attack strategy The introduction of Chip and PIN technology has moved attacks to the merchant terminal or integrated point of sale (POS) solution. In the case of terminals, the terminal is modified by the attacker to record the information on the chip after it is decrypted (skimming). Since most terminals use some form of high-speed network connection, the compromised terminal periodically sends the captured chip data to an attacker anywhere in the world. For POS, attackers compromise the POS station and then obtain the chip data by monitoring the program that processes the Chip 2 white paper and PIN card. Again, since most POS terminals are on a network, attackers have their capture program send the captured card data to their computer. A number of incidents involving the skimming of Chip and PIN cards using tampered software or terminals have been documented. Skimmed cards are typically sold in areas, like Asia and the United States, where magnetic stripes are still used. The incidence of compromised terminals and POS systems has risen significantly since the introduction of Chip and PIN technology. Prior to Chip and PIN, cardholders typically only entered their PIN at ATMs. With the introduction of Chip and PIN, a cardholder’s PIN is now entered in restaurants, supermarkets and anywhere else these cards are accepted. As a result, security analysts have complained that it is more likely that a cardholder’s PIN could be compromised since it is provided in more venues. The credit card industry has responded by changing the PIN pad standard to include shielding around the keypad on the terminal to make observing the entry of the PIN more difficult. However, the shielding is not a perfect solution and PIN entry can still be observed. In addition, terminals with the new shielding have only been available since early 2007 and, given the cost of terminals, the rollout of shielded terminals will take at least five or more years to be completed. functionality the same way regardless of the card used. At a minimum, these backend systems process and transmit cardholder data, but they may also store cardholder data. As a result, these backend systems must comply with the PCI standards. Chip and PIN terminals are no different than their magnetic stripe swiping cousins. They require proper configuration to ensure that they mask cardholder data and transmit transactions securely, so that they comply with the PCI Data Security Standard. They are also required to comply with the PCI PIN Entry Device (PED) standard. Conclusion Chip and PIN reduces face-to-face transaction fraud, but it does not remove all of the risks involved in the use of a credit card. As a result, there is still significant effort required to ensure that an organization’s credit card processing infrastructure is secure and complies with the various relevant PCI standards. For more information, please contact Jeff Hall at 612.376.9280 or jeff.hall@rsmi.com. In addition to direct observation, with the amount of video surveillance implemented by merchants and government entities in Europe, there is a concern that this video surveillance contains a significant amount of footage showing cardholders entering their PINs. It is this video monitoring, coupled with skimming, that law enforcement authorities believe leads to most of the cloned Chip and PIN cards in Europe. Because most Chip and PIN cards still have a magnetic stripe for use outside of Europe, Chip and PIN cards’ magnetic stripes can be cloned and then used anywhere. Chip and PIN cards that are skimmed are typically used in Asia and the United States. PCI compliance The standards promulgated by the PCI Security Standards Council are worldwide in nature. So, regardless of the type of card used, all merchants and acquirers are required to comply with all PCI standards. This is legally enforced through merchant and service provider agreements between these entities and the card brands. Agreements were updated worldwide over the last three to four years to include addendums that require all parties to be PCI compliant. Though Chip and PIN cards and their terminals are different, the integrated POS and the backend systems that authorize and process transactions are not. These systems provide their www.rsmmcgladrey.com 3 RSM McGladrey, Inc. and McGladrey & Pullen LLP have an alternative practice structure. Though separate and independent legal entities, the two firms work together to serve clients' business needs. RSM McGladrey, Inc. is not a licensed CPA firm. RSM McGladrey and McGladrey & Pullen serve clients’ global business needs through their membership in RSM International, the seventh-largest worldwide organization of independent accounting and consulting firms (source: International Accounting Bulletin), with 680 offices and 27,000 professionals in 65 countries. To learn more, call 800.274.3978 or visit www.rsmmcgladrey.com.