Problem Set 7 Solution

probability prediction with static Merton-D-Vine copula model

Pricing Volatility Derivatives with General Risk Functions Alejandro Balbás University Carlos III

Pricing Swing Options and other Electricity Derivatives

Pricing Short-Term Market Risk: Evidence from

Pricing of Interest Rate Derivatives

Pricing Bermudan Style Swaptions Using the Calibrated Hull White

Pricing and Hedging Volatility Derivatives

Pricing and Hedging of swing options in the European electricity and

Pricing and hedging in exponential Lévy models: review of recent

Price Comparison Results and Super-replication: An

Press release

Presentation

留給2006年的一大疑問

甲醇中远期现货交易电子交易合同

“The U.S. economy seems to be firming up as more people are

УДК 336.7 JEL Code G10 С.М. ДЕНЬГА (Полтавський університет

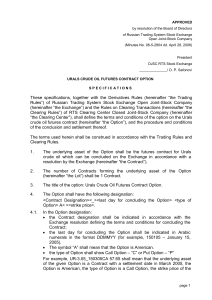

С П Е Ц И Ф И К А Ц И Я

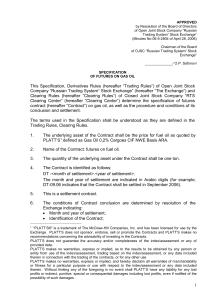

С П Е Ц И Ф И К А Ц И Я

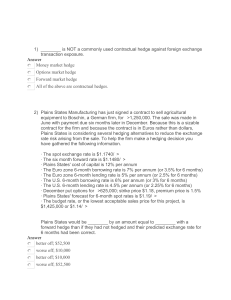

______ is NOT a commonly used contractual hedge against foreign